- February 21, 2018

Federal Home Loan Bank of Dallas Reports Fourth Quarter and Full Year 2017 Operating Results

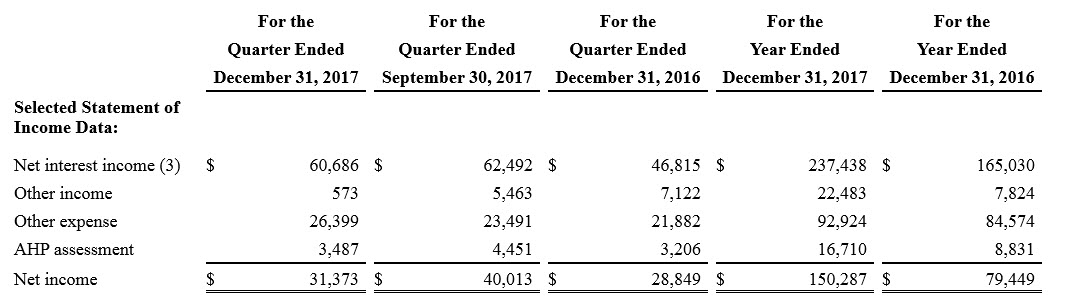

DALLAS, TEXAS, February 21, 2018 - The Federal Home Loan Bank of Dallas (Bank) today reported net income of $31.4 million for the quarter ended December 31, 2017. In comparison, for the quarters ended September 30, 2017 and December 31, 2016, the Bank reported net income of $40.0 million and $28.8 million, respectively. For the year ended December 31, 2017, the Bank reported net income of $150.3 million, as compared to $79.4 million for the year ended December 31, 2016. Net interest income after provision for loan losses for the quarters ended December 31, 2017 and September 30, 2017 and the year ended December 31, 2017 was $60.7 million, $62.5 million and $237.4 million, respectively. In comparison, for the quarter and year ended December 31, 2016, net interest income after provision for loan losses was $46.8 million and $165.0 million, respectively.

The $8.6 million decrease in net income from the third quarter to the fourth quarter of 2017 was attributable in large part to a decrease in the Bank's non-interest income ($4.9 million) and an increase in its non-interest expenses ($2.9 million). The decrease in non-interest income was due largely to a negative swing in the net gains/losses associated with sales of investment securities ($2.5 million) and an unfavorable change in the aggregate net gains and losses associated with the Bank's derivatives and hedging activities and its trading securities portfolio ($2.5 million). The vast majority of the gains and losses associated with the Bank's derivatives and hedging activities and its trading securities portfolio are expected to be transitory. The increase in non-interest expenses was due to a $2.9 million increase in grants and donations that were made to support recovery efforts in the areas impacted by Hurricane Harvey. During the year ended December 31, 2017, the Bank's Hurricane Harvey-related grants and donations totaled $6.5 million.

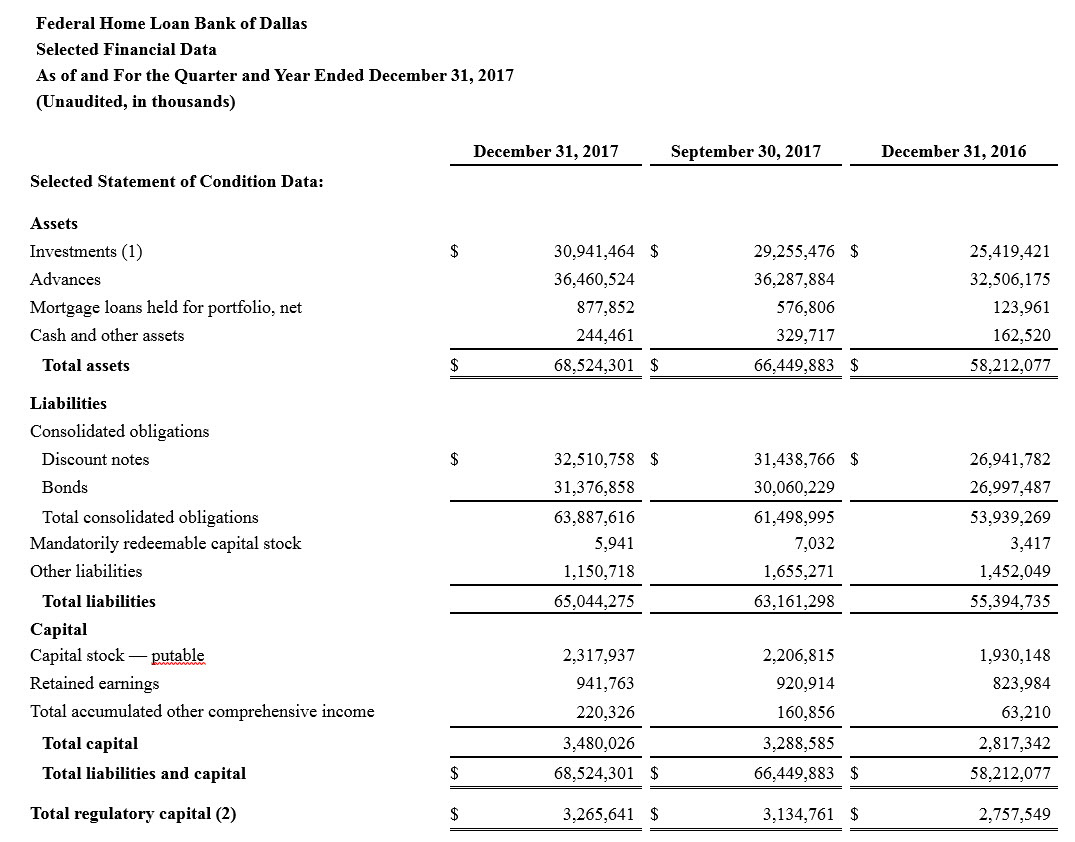

Total assets at December 31, 2017 were $68.5 billion, compared with $66.4 billion at September 30, 2017 and $58.2 billion at December 31, 2016. The $2.1 billion increase in total assets for the fourth quarter was attributable primarily to a $2.4 billion increase in the Bank's short-term liquidity portfolio. For the year ended December 31, 2017, the $10.3 billion increase in total assets was attributable primarily to increases in the Bank's short-term liquidity portfolio ($4.9 billion), advances ($4.0 billion), mortgage loans held for portfolio ($0.8 billion) and long-term investments ($0.6 billion).

Advances totaled $36.5 billion at December 31, 2017, compared with $36.3 billion at September 30, 2017 and $32.5 billion at December 31, 2016. The Bank's mortgage loans held for portfolio totaled $878 million at December 31, 2017, as compared to $577 million at September 30, 2017 and $124 million at December 31, 2016.

The Bank's long-term held-to-maturity securities portfolio, which is comprised substantially of U.S. agency residential mortgage-backed securities (MBS), totaled $1.9 billion at December 31, 2017 as compared to $2.0 billion at September 30, 2017 and $2.5 billion at December 31, 2016. The Bank's long-term available-for-sale securities portfolio, which is comprised substantially of U.S. agency and other highly rated debentures and U.S. agency commercial MBS, totaled $14.4 billion at December 31, 2017 as compared to $15.0 billion at September 30, 2017 and $13.2 billion at December 31, 2016. The Bank also held a $0.1 billion long-term U.S. Treasury Note in its trading securities portfolio at December 31, 2017, September 30, 2017 and December 31, 2016.

The Bank's short-term liquidity portfolio, which is comprised substantially of overnight federal funds sold (including loans to other Federal Home Loan Banks) and reverse repurchase agreements, totaled $14.5 billion at December 31, 2017, compared to $12.1 billion at September 30, 2017 and $9.6 billion at December 31, 2016.

The Bank's retained earnings increased to $942 million at December 31, 2017 from $921 million at September 30, 2017 and $824 million at December 31, 2016. On December 27, 2017, a dividend of $10.5 million was paid to the Bank's shareholders. During the year ended December 31, 2017, the Bank's dividends totaled $32.5 million.

Additional selected financial data as of and for the quarter and year ended December 31, 2017 (and, for comparative purposes, as of September 30, 2017 and December 31, 2016 and for the quarters ended September 30, 2017 and December 31, 2016 and the year ended December 31, 2016) is set forth below. Further discussion and analysis regarding the Bank's results will be included in its Form 10-K for the year ended December 31, 2017 to be filed with the Securities and Exchange Commission.

About the Federal Home Loan Bank of Dallas

The Federal Home Loan Bank of Dallas is one of 11 district banks in the FHLBank System, which was created by Congress in 1932. The Bank is a member-owned cooperative that supports housing and community development by providing competitively priced loans (known as advances) and other credit products to approximately 835 members and associated institutions in Arkansas, Louisiana, Mississippi, New Mexico and Texas. For more information, visit the Bank's website at fhlb.com.

(1) Investments consist of interest-bearing deposits, securities purchased under agreements to resell, federal funds sold, loans to other Federal Home Loan Banks, trading securities, available-for-sale securities and held-to-maturity securities.

(2) As of December 31, 2017, September 30, 2017 and December 31, 2016, total regulatory capital represented 4.77 percent, 4.72 percent and 4.74 percent, respectively, of total assets as of those dates.

(3) Net interest income is net of the provision for loan losses.

Contact Information:

Corporate Communications

Federal Home Loan Bank of Dallas

fhlb.com

214.441.8445